Your Local Mortgage Lender

Located in Destrehan, Louisiana

Personalized Mortgage Experience

Brian Maurice offers personalized service and loan options you'll love. We shop multiple lenders to find the best rate and product for you, getting you into your dream home faster.

With wholesale interest rates and cutting-edge technology, we make the mortgage process seamless. Trust the experts who focus solely on mortgages. Support your local community and experience elite client service.

Let us help you achieve your homeownership dreams!

The Home Loan Process

Mortgage Pre-Approval

Get pre-approved from one of our Loan Officers to see how much you can afford.

House Shopping

Work with a trusted Real Estate Agent to find a home you would like to move into.

Loan Application

Complete your home loan application to get the lending process started.

Don't take my word for it

Mortgage Programs

Experience the best mortgage experience located in Destrehan, Louisiana .

Home Loan Options

Our experienced mortgage advisors will walk you through the best mortgage loan program that will fit your specific scenario.

Conventional Home Loans.

FHA Home Loans.

USDA Home Loans.

VA Home Loans.

Frequently Asked Questions

How often can I refinance my mortgage?

There is no limit to the number of times you can refinance. However, you must qualify every time you apply and there will be costs associated with closing the loan each time.

Can I buy a home if I do not have money for a down payment?

Yes! There are a number of bond programs that offer low or no down payment financing options.

How do I know which mortgage is right for me?

The key to choosing the right mortgage is to understand the range of options and features available to you, as well as your budget, circumstances, and goals. Our licensed mortgage professionals are here to help you navigate that process. The more you know, the more comfortable and confident you will be choosing the best option for you and your family.

How long will the loan process take?

The Truth in Lending Act (TILA) does not permit a lender to close a loan until at least seven (7) business days have passed from the date your application was received. A typical home loan takes 30 days, as a number of third-party services such as appraisals, title work, and credit are required in conjunction with the mortgage process. Once you familiarize your Loan Officer with the details of your specific loan scenario, they will be able to provide you with a more specific timeline.

Will I qualify for a home loan?

The only way to find out is to speak with a qualified mortgage professional. Our Loan Officers have helped numerous clients who didn’t know if they could qualify to become home owners. We take the time to understand your financial situation and long-term financial goals, and then match you with the loan program that best fits your needs. Your approval for a loan may also largely depend on the price of the home you are financing. Getting pre-qualified prior to beginning your home search can give you an idea of what you may be able to afford.

Why do people refinance their mortgages?

Homeowners typically refinance to save money, either by obtaining a lower interest rate or by reducing the term of their loan. Refinancing is also a way to convert an adjustable loan to a fixed loan or to consolidate debts.

How much money will I have to pay upfront to buy a home?

This question does not have a simple, one-size-fits-all answer. The exact amount will depend on the price of the home you buy as well the type of mortgage financing you choose. Depending on your loan program, your down payment could be as much as 20% of the home’s price or as little as 3%, while some loans require no down payment at all.

Can I get a mortgage after bankruptcy?

You may still qualify for a home loan even if you have experienced a bankruptcy. The best way to find out if you qualify is to talk with a Loan Officer to discuss your options. Be sure to bring all paperwork regarding your bankruptcy so your Loan Officer can find the program that best fits your situation.

Should I lock my interest rate now, or wait until we are closer to our closing?

Interest rates fluctuate all day, every day. If an interest rate is good, it may be in your best interest to lock now. If you wait, you run the risk of an increase in rates later. If you are concerned that rates may go down after you lock, contact your Loan Officer to discuss your options. Some programs allow you to lock for an extended period and choose to lower your rate should a better one become available.

Most Recent Blog Updates

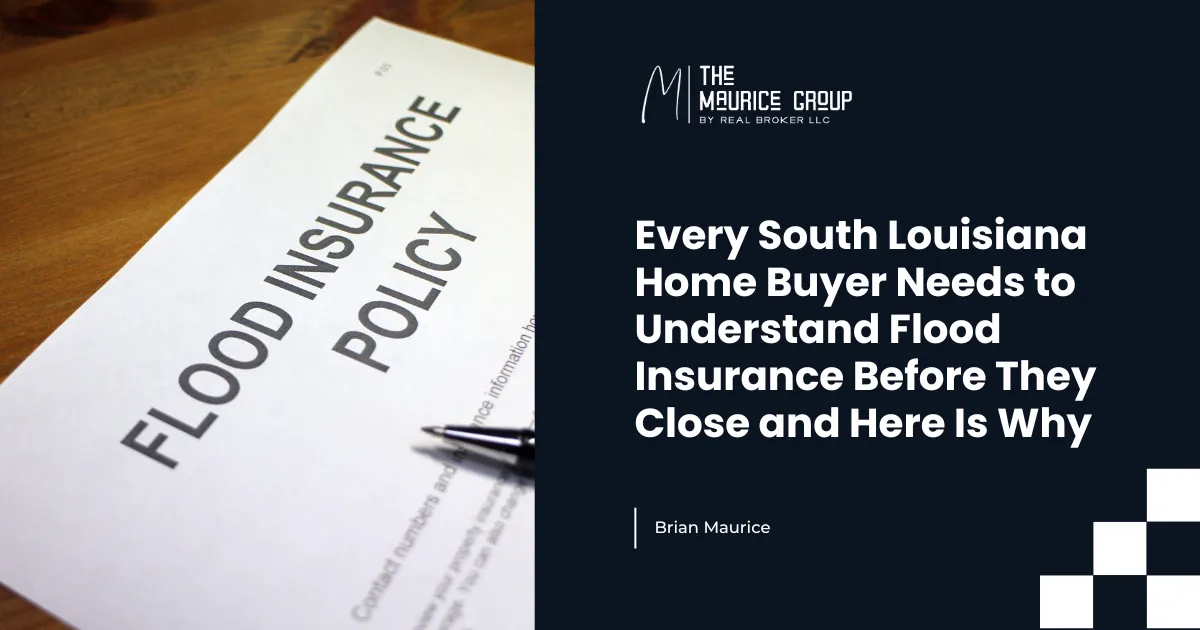

Every South Louisiana Home Buyer Needs to Understand Flood Insurance Before They Close and Here Is Why

The Most Important Thing Louisiana Buyers Need to Know Right Now

If you are buying a home anywhere in Jefferson Parish, Orleans Parish, St. Charles Parish, or really anywhere in South Louisiana this is the conversation you need to have before you close. Not after. Not when the insurance quote comes back two weeks before closing. Before you write the offer.

Flood insurance in South Louisiana is not a secondary consideration or a line item to figure out later. It is a fundamental component of the true cost of homeownership in this region and buyers who do not understand it before they are under contract regularly discover surprises that change the financial picture of the entire transaction.

Why This Matters More in Louisiana Than Almost Anywhere Else

Standard homeowners insurance does not cover flood damage. That is not a Louisiana-specific rule. It is true everywhere in the country. But it matters here more than almost anywhere else because Louisiana receives more rainfall than any other state in the continental United States and sits in one of the most flood-prone regions on the planet.

If your home is in a high-risk flood zone your mortgage lender will require flood insurance as a condition of the loan. No qualifying flood insurance means no closing. Discovering that requirement late in the transaction process when you are already under contract and have already paid for an inspection and appraisal is an expensive and avoidable situation.

Why Zone X Is Not a Free Pass

Here is something that surprises a significant number of buyers. Even if your home falls in Zone X which is classified as moderate to low risk Brian Maurice strongly recommends carrying a flood policy anyway.

The data supports that recommendation. People who own properties outside of high-risk flood zones account for 25 percent of all flood insurance claims nationally. A quarter of all flood claims come from properties that were not in the zones that require coverage. Being outside the mandatory purchase area does not mean being outside flood risk. It means being outside the zone where the government requires you to carry coverage. Those are different things.

What Flood Insurance Actually Costs in South Louisiana

The median flood insurance cost in Louisiana is approximately $1,400 per year but that number varies widely depending on the specific property, its elevation, its location within the parish, and which flood zone designation applies.

A home in the French Quarter or the Irish Channel might carry a flood insurance premium of only a few hundred dollars annually. A home in Lakeview or Bayou Gauche could run $3,000 or more per year. The difference between those two scenarios is several hundred dollars per month in escrow and it affects both the monthly payment and the qualification calculation in ways that need to be understood before the offer is written.

Under FEMA's Risk Rating 2.0 pricing model which replaced the previous rate structure premiums in Jefferson and Orleans parishes have roughly doubled for many homeowners. The new pricing is based on the individual property's specific risk characteristics rather than broad zone designations and the results have been inconsistent in ways that can feel arbitrary. A house on one street may pay dramatically more or less than a comparable house two blocks away.

Your Options Beyond the NFIP

The National Flood Insurance Program is the most widely known source of flood coverage in Louisiana but it is not the only option and comparing it to private flood insurance alternatives could save you a significant amount of money depending on your property.

Private flood insurance has become increasingly competitive and in some cases offers better coverage at lower premiums than the NFIP for certain property types and risk profiles. Getting quotes from both the NFIP and private market alternatives before closing is a step that costs nothing and can produce meaningful savings on an ongoing annual expense that will accompany you for the entire life of your homeownership in South Louisiana.

Factor Flood Insurance Into Your Budget From Day One

As Brian Maurice explains flood insurance is a non-negotiable cost of homeownership in South Louisiana. It is not optional in high-risk zones and it is strongly advisable even where it is not required. The only question is how much it will cost for the specific property you are considering and whether that cost fits within the monthly budget that makes the purchase work financially.

The time to find out that answer is before you write the offer. Not after you are under contract and emotionally invested in a home whose true monthly cost you have not yet fully calculated.

Brian Maurice works with buyers across Jefferson Parish, Orleans Parish, and St. Charles Parish to make sure flood insurance is factored into the budget from the very beginning of the home search rather than discovered as a late-stage surprise. Reach out to Brian Maurice to make sure you understand the full cost of homeownership in South Louisiana before you commit to any specific property.

Sources

FEMA.gov

LouisianaHousingCorporation.gov

NationalFloodInsuranceProgram.gov

GreaterNewOrleansRealtors.com

InsuranceInformationInstitute.org

Mortgage Calculator

See your total mortgage payments using the tool below.

| Year | Interest | Principal | Balance |

|---|

Social Media Links

YouTube